Opinion Article: MINIMUM TAX by CPA Bilal Musani, ACCA

Over the last decade, the Government implemented huge infrastructure projects to spur economic growth and financial stability.

This was largely supposed to ease the tax burden on Kenyans who are already paying huge taxes compared to the other growing nations worldwide, in return for very limited benefits. Fund developments, re-opening of factories, foreign amnesty, Universal Healthcare, Free Schooling, Turkana wind power generation, Oil exploration, Port expansion and of course the SGR were all supposed to ensure economic growth which would ensure that the lives of Kenyans will improve for the better.

Come March 2020, even before our nation was hit with the first COvid 19 case, Treasury is already formulating plans to further tax Kenyans and their businesses. In view of the tax reductions made, the Finance Act is quietly passed in June 2020 and without any hesitance or consideration, Minimum Tax had been introduced.

Minimum Tax is a tax that will be paid by all business in Kenya at the rate of 1% of their gross turnovers.

How the Government plans to implement this tax and convince traders in the country to comply with the new tax will be the challenge. Several associations and organisations are challenging the implementation of the tax and many more stakeholders are expected to challenge and oppose the implementation of these taxes.

How minimum tax will work.

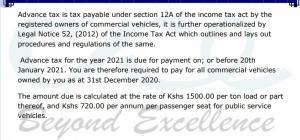

A business trading in Kenya will from 1st January 2021 pay 1% on its turnover.

The Government has been borrowing and borrowing and borrowing. The project impact assessments and financial implications were misstated and miscalculated. The results are that no project has lived up to its expectations financially. Furthermore, political interventions have disabled promising projects such as the implementation of solar power.

Kenyans, who look upon the Government for support and creating of a better living environment will from 1st January feel the effect of the new minimum taxes which will increase the price of commodities as the direct and indirect costs are passed onto the consumers.

The Treasury plans to collect the same tax throughout the cycle of the product in turn taxing the same value over and over. This roll-on effect will result in increased prices.

Manufacture of a product will pay 1% on his sale to a distributor who will once again pay 1% on the same item when selling to a retailer. The retailer is required to again pay 1% when he sells to the final consumer. Along this chain of distribution, the same product, the same cost price has already been taxed 3 times.

The Government has also failed to consider how the minimum tax will affect volume-based businesses. Distributors and commodity importers rely on volume-based trading. A business will have low gross profit margins ensuring high volumes to achieve the desired net profits. Commodities trade and distribution work on margins close to 1% in some cases. In order to make the business profitable, companies and traders will resort to cost-cutting. Redundancies, pay cuts and job cuts will be the order of the day.

Over the last few years, the Government has implemented policies to allow banks to provide better credit facilities and to encourage lending by banks. Late payment of taxes results to interest and penalties charged monthly. Banks that have provided loans and overdraft facilities to businesses will witness further loan applications as well as defaults of the loans. A business will race to borrow from banks in order to pay the required taxes, most businesses have extended credit terms post covid. In addition to the cash outflows, businesses will experience, interest and finance costs are expected to further eat into profits.

Kenya, as a nation has been investing heavily in infrastructure, revising and implementing new trade policies with other nations to increase its export trade as well as provide competitive prices internationally. With the implementation of the minimum tax, Kenya’s exports are going to be pricy and less competitive which will discourage exports from Kenya. With lesser US Dollars flowing into the economy than the US Dollars being paid out as loans and for imports, we may see the US Dollar crossing the 120 shilling mark sooner than later.

A recent drive along the Mombasa – Nairobi highway and the Coastal business environment will already tell you tales of a struggling region after the SGR. Furthermore, the tourism sector has almost but nearly stood still during the COVID -19 pandemic. The little foreign currency that is expected from the few tourists willing to take a chance and holiday in Kenya may also disappear as our neighbours Tanzania will be a cheaper destination to fly to.

Kenya is a net importer, as a farming nation, it still cannot meet the food demand for its people. A nation blessed with rich volcanic soil, suitable temperatures and massive underground water reserves. Today, Kenya imports rice, sugar, wheat and even maize. Our policies have over the years shifted from self-sustainment to economic colonization. Our products locally have become pricier than products imported and we are certain to stop manufacturing in the coming few years. The minimum tax will make food prices rise in an already low supply market, affordability will be a new status amongst the low income earning people who are the largest of the population.

Where will our investments come from? I recall a conversation I had with an investor trying to set up a lipstick manufacturing plant in Kenya. His concern was the costs in the country were so high that it was cheaper for him to import the final product and distribute it locally. Investors are setting base in Rwanda and Ethiopia which provides them with the tax benefits as well as a cheaper source of fuel. With the implementation of the minimum tax, investors are unlikely to recover their investments faster and the costs of their products will discourage any exports from Kenya.

The Government has also passed the revised PAYE rates effective January 2021, Kenyans are expected to be taxed further on their incomes over Kshs. 24,000 per month. There will be lesser take-home pay for the middle-income earners, lesser money to spend and with an expected price increase from the minimum tax implementation I see 2021 for Kenyans being far much worse than what we experienced in 2020.

The target set by the Government to collect taxes by implementing this tax may yet not be realized. The effect of the same will be realized in other sectors of Government revenues. Pay As You Earn collections will be reduced as more and more businesses reduce staff. VAT will reduce as more and more business close shop to divert investments in sectors which are much profitable (Government Bonds and Treasury Bills), county revenues will reduce as businesses close and relocate to other countries, duties and imports will fall as lesser people will be willing to invest into Kenya.

We pray that the fight is joined in by all relevant stakeholders but for the few that are in it, Kenyans are hoping and praying for your victory.

This tax will have an adverse effect on businesses, including deterring startups, increasing costs to consumers and increase cash flow constraints, which will consequently push struggling entities to reduce operations or worse, prematurely close. This will lead to loss of jobs and take the economy into a downward spiral of contraction – Mr Mucai Kunyiha, KAM Chairman.

The timing to impose such taxes on businesses is ill-advised. This unpredictability will overburden businesses and increase costs. We need to discipline public spending. Our debt is a spending problem and not a tax problem. This is a cynical way of collecting taxes because businesses will be taxed whether or not they make profits – Mr Owino, CEO Institute of Economic Affairs.

Unfavourable tax policies not only discourage investment and growth, but they are also a disincentive to exporters, which in the long run dilutes our competitiveness. The government does not generate revenue. Revenue comes from businesses and individuals. Therefore, for any economy to grow, the Government must make it conducive for business to operate effectively – FCPA Rose Mwaura Institute of Certified Public Accountants of Kenya (ICPAK) National Chair.